Financial Education/Information

Credit Score

A credit score influences the credit that's available to you and the terms that lenders offer you. It's a vital part of your credit health.

The most widely used credit score is the FICO Score, the credit score created by Fair Isaac Corporation. Lenders use the FICO Score to help make credit decisions. Fair Isaac calculates the FICO Score based solely on information in consumer credit reports maintained at the credit reporting agencies.

FICO credit scores range from 300 to 850. The FICO Score is calculated by a mathematical equation that evaluates many types of information from your credit report, at that agency. Please see pie chart below for what percentages TransUnion utilizes to determine a FICO score. By comparing this information to the patterns in hundreds of thousands of past credit reports, the FICO Score estimates your level of future credit risk. The higher the score, the lower the risk. But no score says whether a specific individual will be a "good" or "bad" customer.

The big three credit bureaus, TransUnion, Equifax and Experian developed their own credit score as an alternative to FICO called VantageScore and began marketing it in 2006. The VantageScore is calculated differently than the FICO score. Furthermore, the VantageScore 2.0 utilized a score range of 501-990 but the newer VantageScore 3.0 utilizes a score of 300-850. It is important for you to know what score you are being presented and in the case of VantageScore what version. The VantageScore and FICO score can vary widely. For more information about the VantageScore 3.0 model please visit here.

STRCP Credit Reporting

The Siletz Tribe Revolving Credit Program submits monthly reports of all active STRCP loans to TransUnion Credit Agency. Should you have any questions or concerns about your Siletz Tribe Revolving Credit Program loan credit reporting please don't hesitate to contact Siletz Management, LLC at 1-541-351-9154. Our office hours are Monday through Friday 8:00am to 4:30pm except holidays.

TransUnion Credit Report Item Dispute

Should you want more information on how to dispute a credit item on your report through TransUnion you can go to the TransUnion Credit Disputes FAQs page.

You can also submit disputes to TransUnion online, by phone or by mail:Online: Online dispute submission process

Phone: Call 1-800-916-6800. Hours are 8:00am to 11:00pm Eastern Time Monday through Friday.

Mail to:

- TransUnion, LLC

- Consumer Dispute Center

- P.O. Box 2000

- Chester, PA 19022

FICO Credit Score Percentage Breakdown

- Payment History

- Amount you owe

- Length of Credit history

- New credit opened

- Types of credit opened

VantageScore 3.0 Score Influences

Extremely Influential

Payment History: Make sure you pay your bills on time.

Highly Influential

Age and type of credit: It's helpful to maintain a mix of accounts (credit cards, auto, mortgage) overtime to improve your score.

% of credit limit used: Focus on keeping revolving balances low, under 30% of credit limit.

Moderately Influential

Total balances/debt: Best to reduce the amount of debt you owe.

Less Influential

Recent credit behavior and inquiries: Don't open too many new accounts too quickly.

Available credit: Only open the amount of credit you need.

Credit Score Information

Do you know what your credit score is or what it means?

Topics covered include understanding credit score basics, credit report basics, preventing fraud, and credit advice.

Looking for more information on how to repair your credit through a credit repair company?

Experian Credit Educator

STRCP highly recommends all loan applicants look at utilizing the "Gain a Better Understanding of Your Credit with Experian Credit Educator" service offered by Experian. For $39.95 you will receive a one time, one-on-one credit education session including:

- A copy of your Experian credit report and score

- A step-by-step walkthrough of your personal credit report

- Specific examples of actions that may increase your credit score

- Insight for future decision in personal credit management

The three major credit bureaus:

Five C's of Credit

- Character: Credit History

- Capacity: Repayment sources, debt to income ratio

- Capital: Personal investment, alternative repayment sources

- Collateral: Personal valuables to guarantee repayment

- Conditions: Situations that affect repayment

Free Annual Credit Report

Under Federal Law everyone is entitled to receive one free credit report from Experian, Equifax and TransUnion every 12 months. You may receive a credit report from all three at one time or any single one of them at a time. In other words, you may receive a free report from all three bureaus together or get a report from Equifax and three months later request one from TransUnion. The free credit reports can be requested through the website linked below, by phone or by mail. Free Credit Report

There is no reason to pay any fee for an annual copy of your credit report from each of three credit bureaus.

Be aware that many websites offer to give you a "free" credit report/score by signing you up for a "free" trial offering a monthly based monitoring service that automatically begins charging your credit card after a short free trial period. Most often, when a website requires you to input credit card information to receive your "free" report/credit score you often are authorizing that company to deduct a fee from your account.

One such example is Free Credit Report.com. From their website homepage they state:

- *IMPORTANT INFORMATION When you order your $1 Credit Report and FREE Score here, you will begin your 7-day trial membership in freecreditreport.com. If you don't cancel your membership within the 7-day trial period**, you will be billed $14.99 for each month that you continue your membership. You may cancel your trial membership anytime within the trial period without charge. Click here to access your free annual credit report available under federal law. Calculated on the PLUS Score model, your Experian Credit Score indicates your relative credit risk level for educational purposes and is not the score used by lenders. Learn more.

Credit Karma

Credit Karma ™ is a completely free pro-consumer service dedicated to demystifying the credit landscape. With their credit simulators, free credit scores, credit advice, and credit score comparisons, their goal is to empower consumers to more actively manage their credit and their financial health. Please note Credit Karma utilizes the VantageScore 3.0 format and reports a score from Equifax and TransUnion. This score is from a "soft pull" (doesn't affect your credit score unlike a "hard pull" report like the one pulled by the STRCP or other creditors) and does not necessarily translate to the same FICO score. Also, many major credit card companies offer free "soft pull" credit FICO score reporting as a benefit to having their charge card.

Learn More

Personal Budgeting

If you plan to apply for credit through STRCP or another financial institution it is important you understand the impact it will have on your finances. This includes knowing what the monthly payment is (and the interest rate) and whether you can afford to make the payments. One issue that often occurs for people when they purchase cars, for example, is they don't take the monthly insurance premium into consideration when determining whether they can afford the monthly payments. To help you understand whether you can afford a STRCP loan we have a Personal Income & Expenses Template in Microsoft Office Excel or PDF format to help you take control of your personal budgeting. The STRCP Board and the STRCP Credit Administrator highly recommends all STRCP loan applicants utilize this template to determine if they can afford an additional loan payment.

Please note the second page of the PDF (Tab two (2) on the Excel Worksheet) where you can fill out a Goals Worksheet. Whether you are saving for a car, wanting to start a business or save for college it is important to develop and prioritize your savings goals.

One of the major reasons many new businesses fail is a lack of reserve capital (cash) and/or not enough free operating capital (cash) for the small business owner to pay his/her personal living expenses. Utilizing this template can help reduce financial surprises (and you may be surprised at where most of your income actually goes in any given month!).

Although not a requirement, you may fill out and provide a copy of your personal budget to the STRCP Board as part of your application packet.

Your Equal Credit Opportunity Rights (ECOA)

You use credit to pay for education or a house, a remodeling job or a car, or to finance a loan to keep your business operating.

The Federal Trade Commission (FTC), the nation’s consumer protection agency, enforces the Equal Credit Opportunity Act (ECOA), which prohibits credit discrimination on the basis of race, color, religion, national origin, sex, marital status, age, or because you get public assistance. Creditors may ask you for most of this information in certain situations, but they may not use it when deciding whether to give you credit or when setting the terms of your credit. Not everyone who applies for credit gets it or gets the same terms: Factors like income, expenses, debts, and credit history are among the considerations lenders use to determine your creditworthiness.

The law provides protections when you deal with any organizations or people who regularly extend credit, including banks, small loan and finance companies, retail and department stores, credit card companies, and credit unions. Everyone who participates in the decision to grant credit or in setting the terms of that credit, including real estate brokers who arrange financing, must comply with the ECOA. See here for more information (Source)

Summary of basic provisions of the ECOA

- Discourage you from applying or reject your application because of your race, color, religion, national origin, sex, marital status, age, or because you receive public assistance.

- Consider your race, sex, or national origin, although you may be asked to disclose this information if you want to. It helps federal agencies enforce anti-discrimination laws. A creditor may consider your immigration status and whether you have the right to stay in the country long enough to repay the debt.

- Impose different terms or conditions, like a higher interest rate or higher fees, on a loan based on your race, color, religion, national origin, sex, marital status, age, or because you receive public assistance.

- Ask if you’re widowed or divorced. A creditor may use only the terms: married, unmarried, or separated.

- Ask about your marital status if you’re applying for a separate, unsecured account. A creditor may ask you to provide this information if you live in “community property” states: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. A creditor in any state may ask for this information if you apply for a joint account or one secured by property.

- Ask for information about your spouse, except:

- if your spouse is applying with you;

- if your spouse will be allowed to use the account;

- if you are relying on your spouse’s income or on alimony or child support income from a former spouse;

- if you live in a community property state.

- Ask about your plans for having or raising children, but they can ask questions about expenses related to your dependents.

- Ask if you get alimony, child support, or separate maintenance payments, unless they tell you first that you don’t have to provide this information if you aren’t relying on these payments to get credit. A creditor may ask if you have to pay alimony, child support, or separate maintenance payments.

- Consider your race, color, religion, national origin, sex, marital status or whether you get public assistance.

- Consider your age, unless:

- you’re too young to sign contracts, generally under 18;

- you’re at least 62, and the creditor will favor you because of your age;

- it’s used to determine the meaning of other factors important to creditworthiness. For example, a creditor could use your age to determine if your income might drop because you’re about to retire;

- it’s used in a valid credit scoring system that favors applicants 62 and older. A credit scoring system assigns points to answers you give on credit applications. For example, your length of employment might be scored differently depending on your age.

- Consider whether you have a telephone account in your name. A creditor may consider whether you have a phone.

- Consider the racial composition of the neighborhood where you want to buy, refinance or improve a house with money you are borrowing.

- Refuse to consider reliable public assistance income the same way as other income.

- Discount income because of your sex or marital status. For example, a creditor cannot count a man’s salary at 100 percent and a woman’s at 75 percent. A creditor may not assume a woman of childbearing age will stop working to raise children.

- Discount or refuse to consider income because it comes from part-time employment, Social Security, pensions, or annuities.

- Refuse to consider reliable alimony, child support, or separate maintenance payments. A creditor may ask you for proof that you receive this income consistently.

- Have credit in your birth name (Mary Smith), your first and your spouse’s last name (Mary Jones), or your first name and a combined last name (Mary Smith Jones).

- Get credit without a cosigner, if you meet the creditor’s standards.

- Have a cosigner other than your spouse, if one is necessary.

- Keep your own accounts after you change your name, marital status, reach a certain age, or retire, unless the creditor has evidence that you’re not willing or able to pay.

- Know whether your application was accepted or rejected within 30 days of filing a complete application.

- Know why your application was rejected. The creditor must tell you the specific reason for the rejection or that you are entitled to learn the reason if you ask within 60 days. An acceptable reason might be: “your income was too low” or “you haven’t been employed long enough.” An unacceptable reason might be “you didn’t meet our minimum standards.” That information isn’t specific enough.

- Learn the specific reason you were offered less favorable terms than you applied for, but only if you reject these terms. For example, if the lender offers you a smaller loan or a higher interest rate, and you don’t accept the offer, you have the right to know why those terms were offered.

- Find out why your account was closed or why the terms of the account were made less favorable, unless the account was inactive or you failed to make payments as agreed.

A good credit history — a record of your bill payments — often is necessary to get credit. This can hurt many married, separated, divorced, and widowed women. Typically, there are two reasons women don’t have credit histories in their own names: either they lost their credit histories when they married and changed their names, or creditors reported accounts shared by married couples in the husband’s name only.

If you’re married, separated, divorced, or widowed, contact your local credit reporting companies to make sure all relevant bill payment information is in a file under your own name. Your credit report includes information on where you live, how you pay your bills, and whether you’ve been sued, arrested or filed for bankruptcy. National credit reporting companies sell the information in your report to creditors, insurers, employers, and other businesses that, in turn, use it to evaluate your applications for credit, insurance, employment, or renting a home.

The Fair Credit Reporting Act (FCRA) requires each of the three nationwide credit reporting companies - Equifax, Experian, and TransUnion - to give you a free copy of your credit report, at your request, once every 12 months. To order your report, visit annualcreditreport.com or call 1-877-322-8228.

- Complain to the creditor. Sometimes you can persuade the creditor to reconsider your application.

- Check with your state Attorney General’s office to see if the creditor violated state equal credit opportunity laws.

- Consider suing the creditor in federal district court. If you win, you can recover your actual damages and be awarded punitive damages if the court finds that the creditor’s conduct was willful. You also may recover reasonable lawyers’ fees and court costs. Or you might consider finding others with the same claim, and getting together to file a class action suit. An attorney can advise you on how to proceed.

- Report violations to the appropriate government agency. If you’ve been denied credit, the creditor must give you the name and address of the agency to contact.

A number of federal agencies, including the FTC, share enforcement responsibility for the ECOA. Visit the Consumer Financial Protection Bureau or HelpWithMyBank.gov, a site maintained by the Office of the Comptroller of the Currency, for answers to frequently-asked questions on topics like bank accounts, deposit insurance, credit cards, consumer loans, insurance, mortgages, identity theft, and safe deposit boxes, and for other information about federal agencies that have responsibility for financial institutions

Credit Reports

The Siletz Tribe Revolving Credit Program submits monthly reports of all active STRCP loans to TransUnion. Please see below for answers to common questions. Should you have any questions or concerns about your Siletz Tribe Revolving Credit Program loan credit reporting to the credit bureau(s) by Siletz Management, LLC please don't hesitate to call us at 1-877-564-7298. Our office hours are Monday thru Friday 8:00am to 4:30pm.

Frequently Asked Credit Reporting Questions

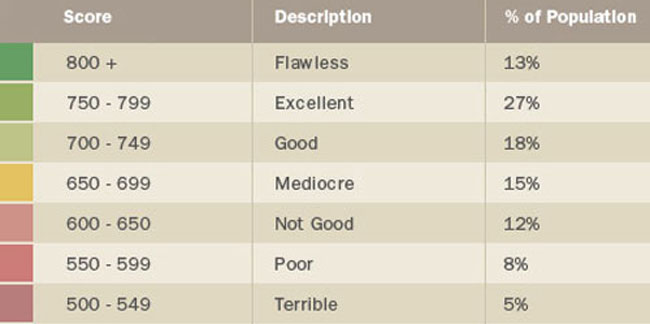

A. A good credit score depends on the scoring system used by your particular lender. Different scoring systems use different scales. However, if you have a good credit score from one of the credit reporting agencies, you are likely to have a good credit score with your lender.

- Most credit scores fall between 600 and 750.

- A score above 700 usually suggests good credit management and above 750 excellent credit management (and the lowest interest rate).

- You may get different scores from each of the three credit bureaus (STRCP utilizes the TransUnion FICO score to determine loan eligibility). (myFico, 2014)

A. The information that impacts a credit score varies depending on the score being used. Credit scores are affected by elements in your credit report, such as:

- Payment history. Number and severity of late payments (a very large part of Experian’s formula for determining a credit score).

- Amounts you owe.

- Length of credit history.

- New credit opened.

- Types of credit you have.

- Other things that may impact your credit score are "hard pull" credit score inquiries and Public records Source.

A. It depends on the type of negative information. Here's the basic breakdown of how long different types of negative information will remain on your credit report:

- Late payments: 7 years.

- Bankruptcies: 7 years for completed Chapter 13 bankruptcies and 10 years for Chapter 7 bankruptcies.

- Foreclosures: 7 years.

- Collections: Generally, about 7 years, depending on the age of the debt being collected.

- Public Record: Generally 7 years, although unpaid tax liens can remain indefinitely.

Keep in mind: For all of these negative items, the older they are the less impact they are going to have on your FICO® score. For example, a collection that is 5 years old will hurt much less than a collection that is 5 months old (myFico, 2014).

Each state has different rules and statutes comprising their fair debt collection laws. Please click here for Oregon’s Debt Collection information.

Disclaimer: All information found on this website is not considered legal or financial advice and is for informational purposes only. The outcome utilizing this information is not guaranteed by STBC, STRCP, SMI and/or CTSI or their resppective officers. All fillable PDFs require a compatible PDF reader program. If you don't have a compatible reader please click link below depending on your Operating System (OS). Please remember to uncheck any "Optional Offer" on the Adobe webpage before downloading Adobe Reader for Windows unless you want the free McAfee Security Scan Plus utility.

Adobe Reader for Windows Adobe Reader for Apple OSX- Do not pay off any debt or account on your credit report without further investigation and/or attempt to have its status changed on your credit report. Having a negative paid item on your credit report is not necessarily beneficial. Second, make sure you communicate with creditors via USPS Certified Mail to have proof of receipt. Some potential steps for you to improve your credit score are below.

-

Submitting a Debt Validation Letter to the Creditor is an option under the Fair Debt Collection Practices Act (FDCPA).

Debt Validation Letter Fillable PDF -

If there is no response from the creditor for more than 30 days validating the debt, the submission of a follow up letter informing the creditor they are in violation of the FDCPA is an option.

30 Day No Response Debt Validation Letter Fillable PDF -

If the creditor provides validation for the debt and/or you acknowledge the debt and wish to pay it off you have the option to submit a Pay to Delete request to the Creditor. This letter will acknowledge your willingness to pay the debt if the creditor/debt collector agrees to change the status of the account on your credit reports (Experian, TransUnion, Equifax) to "Pays As Agreed" (or remove from your report) and to agree the account is not resold/transferred to any other collection agency. The advantage of the creditor agreeing to change the status of the account to “Pays as Agreed” is that it will no longer be a negative item on your report. It is important an authorized representative from the creditor signs off on this letter. It is important to remember the creditor may not agree to change the negative item to "Pays as Agreed" on the report. It is also important to note whether you are negotiating with the original creditor or a collection agency. Be cautious in dealing with collection agencies.

For example, never give them your bank information electronic or otherwise.

Pay for Delete Fillable PDF

A. There are number of steps you can take to help prevent credit card fraud and quickly report it if it does happen. The State of Oregon Division of Finance and Corporate Securities (DFCS) has webpages dedicated to helping you as the consumer. For those tribal members located in other states their state websites most likely will have similar information and action steps as they are often identical. Actions include:

- Obtaining a security freeze which serves as a deterrent against identity theft.

- Placing a fraud alert on your credit report. You can place a fraud alert on your credit report which requires creditors to call you directly before extending credit. However, this will not necessarily stop creditors from checking your credit report. A security freeze is stronger than a fraud alert because it prevents anyone from accessing your credit file for any reason unless you instruct the credit reporting agencies to unfreeze your report. You can contact any one of the three credit agencies (Equifax, Experian or TransUnion) to place a fraud alert.

If you believe you are a victim of identity theft:

- File a police report to document the crime for your creditors. Contact your local police department or sheriff's office. Make sure you get a copy or the report number.

- Report the theft to the Federal Trade Commission 1-877-438-4338 or FTC Complaint Assistant.

- Contact all your creditors such as your bank, credit union, credit card company, cell phone provider, and other utilities. (Store all their toll-free, 24/7 customer service phone numbers in your cell phone contact list or write down and put in a secure place.)

- Carefully read your monthly statements (credit card, bank, cell phone) for any unauthorized charges.

- Get your free annual credit reports.

- Additional links regarding identity theft include FTC.Gov Identity Theft and Being Smart Online.

Credit Repair Companies

You may have heard the ads on the radio about companies promising to fix your credit so you can get that low interest loan for a new car etc. Many of these companies are scams trying to take your money with no guaranteed results. However, there are a few legitimate credit repair companies. There is no magic formula to raise your credit score fast but there are times when a credit repair company can give your score a bump and/or negotiate for you to remove negative items from your credit report. The information below can be found at Huffington Post Credit Repair Service Blog. Always investigate and be cautious using any credit repair company. The bottom line is credit repair through a credit repair company is not usually guaranteed but if you utilize a company with a good reputation and money-back guarantee, understand the risks you can avoid having negative consequences. STBC, SMLLC and CTSI do not endorse any of these companies. They are examples only. Please evaluate each one.

Frequently Asked Credit Reporting Questions

A. If you have legitimate errors on your credit report: The main function of any credit repair service is to remove errors from your credit report. These could range from errors in reporting from lenders to simple errors in your personal information. A good amount can actually effect your credit, so if you believe there are errors in your credit report, you can benefit from a credit repair company correcting those errors for you.

If you have errors that can't be verified: A little known fact about your credit report is that every detail in the report needs to be verifiable. For example, if you have a negative item on your credit report from a lender who was bought or went out of business, there is a chance that if the credit bureaus were to call to verify the information on your report, they would get no answer. In that case, they are required to remove it from your credit report. This is a loophole that credit repair services will use to raise your score.

If your lenders are willing to work with credit repair agencies: The credit repair agencies that have been doing this for a while know the tricks of the trade, so they have the experience to negotiate with your lenders on your behalf. Does this always work? No. Some lenders don't like working with credit repair services. Some lenders aren't willing to negotiate. However, for the lenders who are willing to listen, this is a good way for credit repair services to raise your score.

A. There are a lot of credit repair companies out there and a lot of scams that go with them, so how can you find the more reliable ones? Look for three things: longevity, reputation and money-back guarantee. Three companies to start with:

Sky Blue Credit Repair

They have an "A+" rating from the BBB, which is a top score from a credit repair company. SkyBlue is also one of the only credit repair services that offers a full 90-day refund (as of November 15, 2015) no matter what the reason, which is unheard of in credit repair. You can sign up on their website or call 1-888-534-1510 for more information. As of November 15, 2015 they charge $59.95/month.

Lexington Law Company

The best part about Lexington Law is that it is an actual law firm that specializes in credit law, which means they know what they are doing when dealing with lenders. It also has an "A" rating from the BBB, and has been around longer than most other credit repair services. Lexington Law is on the cheaper end at $59.95 a month, with a $99.95 initial fee, which includes all of the bells and whistles that come along with their credit repair plan, including a guarantee. Guarantee? Lexington Law doesn't charge you anything until they've completed all the work that they agreed to.

CreditRepair.com

CreditRepair.com has a relationship with TransUnion, so they can actually pull your credit score for you, which is extremely helpful. They also have an "A" rating from the BBB. The only downside to CreditRepair.com is the cost. They charge $89.95 a month, although they don't have an initial fee like most other credit repair services. With the $89.95, you get your standard credit repair services, as well as monthly credit monitoring, a score tracker and analysis, mobile apps and text and email alerts.

Understanding total repayment cost to you

It is important to understand the total interest you will be required to pay in addition to the principal.

For example: If you take out a STRCP consumer loan of $3,030.00 with a 24 month repayment term with a 8% interest rate:

- Your monthly payments will be approximately $137.22.

- Total interest you will pay on loan is $293.28.

- Total amount owed to creditor is $3,293.28.

Impact of Credit Score & Interest Rate on Cost of Loan

The interest rate on your loan is critical in determining how much you owe and most creditors determine your interest rate by your credit score.

This is an example of two different applicants applying for an identical car loan outside of STRCP for $20,000.

| Applicant 1 | Applicant 2 | |

|---|---|---|

| Credit Score | 770 | 530 |

| Length of Loan | 60 months | 60 months |

| Loan Amount | $20,000 | $20,000 |

| Interest Rate | 2.49% | 18.99% |

| Interest Owed | $1,291.54 | $11,122.06 |

| Total Amount for Pay Off | $21,291.54 | $31,122.06 |

Applicant 2 will pay $9,830.52 more for the same car due to their lower credit score & higher interest rate!

Business Planning

Starting a new business is an exciting and sometimes scary proposition. There are many questions for you to consider ranging from your business structure, partners, funding, taxes, insurances etc. This page is designed to help you address some of these concerns so the scary proposition part goes away and you are left only with the excitement of starting or improving your business. STBC and STRCP strongly encourages every new (and existing) business owner to review this information. Some of the information you may already know and some of it may be new. Please don't hesitate to contact the STRCP Credit Administrator if you have any questions.

The Small Business Administration is a great online resource for new and existing business owners. Most of the information below is directly derived from their website.

General Questions

A. The SBA has the following 20 questions that are a good start:

- Why am I starting a business?

- What kind of business do I want?

- Who is my ideal customer?

- What products or services will my business provide?

- Am I prepared to spend the time and money needed to get my business started?

- What differentiates my business idea and the products or services I will provide from others in the field?

- Where will my business be located?

- How many employees will I need?

- What types of suppliers do I need?

- How much money do I need to get started?

- Will I need to get a loan?

- How soon will take before my products or services are available?

- How long do I have until I start making a profit

- Who is my competition?

- How will I price my product compared to the competition?

- How will I setup the legal structure of my business?

- What taxes do I need to pay?

- What kind of insurance do I need?

- How will I manage my business?

- How will I advertise my business?

A. Absolutely! Things to think about when asking this question include:

- Comfortable taking risks: Being your own boss also means you're the one making tough decisions. Entrepreneurship involves uncertainty. Do you avoid uncertainty in life at all costs? If yes, then entrepreneurship may not be the best fit for you.

- Independent: Entrepreneurs have to make a lot of decisions on their own. If you trust your instincts - and you're not afraid of rejection every now and then - you could be on your way to being an entrepreneur.

- Persuasive: You may have the greatest idea in the world, but if you cannot persuade customers, employees and potential lenders or partners, you may find entrepreneurship to be challenging. If you enjoy public speaking, engage new people with ease and find you make compelling arguments grounded in facts, it’s likely you’re poised to make your idea succeed.

- Able to negotiate: As a small business owner, you will need to negotiate everything from leases to contract terms to rates. Polished negotiation skills will help you save money and keep your business running smoothly.

- Creative: Are you able to think of new ideas? Can you imagine new ways to solve problems? Entrepreneurs must be able to think creatively. If you have insights on how to take advantage of new opportunities, entrepreneurship may be a good fit.

- Supported by others: Before you start a business, it’s important to have a strong support system in place. You’ll be forced to make many important decisions, especially in the first months of opening your business. If you do not have a support network of people to help you, consider finding a business mentor. A business mentor is someone who is experienced, successful and willing to provide advice and guidance. Read the Steps to Finding a Mentor article for help on finding and working with a mentor.

A. 10 steps to start a business include:

- Write a business plan.

- Get business assistance and training.

- Choose a business location.

- Finance your business.

- Determine the legal structure of your business.

- Register a business name (such as "Doing Business as" - DBA).

- Get a Tax Identification Number (TIN).

- Register for state and local taxes (if applicable). Members who have their business on trust/reservation land have different taxation requirements.

- Obtain business licenses and permits.

- Understand employer responsibilities.

Management

A. There are number of different legal business structures that each have their own advantages and disadvantages.

- Sole Proprietorship: A sole proprietorship is the most basic type of business to establish. You alone own the company and area responsible for its assets and liabilities. Learn more.

- Limited Liability Company: An LLC is designed to provide the limited liability features of a corporation and the tax efficiencies and operational flexibility of a partnership. Learn more.

- Cooperative: People form cooperatives to meet a collective need or to provide a service that benefits all member-owners.Learn more.

- Corporation: A corporation is more complex and generally suggested for larger, established companies with multiple employees.Learn more.

- Partnership: There are several different types of partnerships, which depend on the nature of the arrangement and partner responsibility for the business. Learn more.

- S Corporation: An S corporation is similar to a C corporation but you are taxed only on the personal level. Learn more.

A. There are number of different questions that need to be answered after you determine what business structure you want to utilize for your business. Most entrepreneurs or small business owners start with a Limited Liability Company or Sole Proprietorship. The Limited Liability Company most often offers the advantage of limited personal liability of a corporation without the complexities of corporate administration. STBC does not reccomend utilization of a sole proprietor business structure. For example, your personal assets (such as your personal property to include house or car etc.!) could be sought by creditors if you default on a business debt. However, depending on the type of business you want to operate, a corporation may be a better fit (especially if you want to raise capital through issuance of stock (shares of ownership of the corporation). However, as with all information on this website, STBC recommends you consult an attorney and/or certified financial planner/accountant when starting a new business and assumes no liability.

Things you need to consider when starting a Limited Liability Company (LLC):

While a LLC is less complex to administer than a corporation there are still requirements that may vary from state to state. For Oregon, the LLC is required to file an Annual Report.

A. Things you need to consider when starting a Corporation:

- Like the LLC, the Corporation is formed at the state level. For Oregon you would visit here. The state agency where you need to register your corporation will vary from state to state.

- Choose the corporation's name. Please note you need to ensure you do not choose the same business name as another corporation already registered in the state. For Oregon, you can do a business name registry search here.

- Designate a registered agent. Each state requires corporations to have a designated registered agent to receive service of process and office mail on a business' behalf. Typically a registered agent must be a business or individual residing in teh state where the corporation is being formed.

- Complete the Articles of Incorporation. For more information on the Articles of Incorporation from the Secreatry of State of Oregon please visit here.Please see the link above to a sample Oregon Secretary of State supplied Article of Organization. Please click here for an example Articles of Incorporation pdf document and visit herefor more information on what is normally required in an Articles of Incorporation. Please note, a corporation is more complex to admnister than an LLC and requires Shareholder meetings, Board of Director's meetings (with minutes kept on record), Corporate resolutions, shareholder resolutions & Board of Director resolutions as well as issuance of stocks. Much of this information is sourced from the Northwest Registered Agent, LLC website and is a very good resource to gather more information about how business structures work.

A.

Here are some simple asset protection strategies for the small business owner utilizing a Limited Liability Company (or corporation) may want to do to reduce their personal liability according to Northwest Registered Agent, LLC:

- Do not own things personally. (That you utilize for your business).

- Own your vehicle(s) in an LLC name to keep your personal name(s) off the DMW records.

- Own your home in an LLC name to keep your personal name(s) of the county assessor records.

- Own your investments in an LLC name.

- If you own a business, have one business entity that transacts business with your clients, and one for the assets of the business. The asset-holding LLC charges the business entity that is out there every day to use its assets. In theory, the business entity doing the work doesn't really own anything.

It is important to keep in mind that just having an LLC does not fully absolve its members of personal liability automatically. Please read here for more information. While you can incorporate or create a Limited Liabilty Corporation on your own there are companies such as Northwest Registered Agence, LLC that charges a variety of fees to assist you in forming an LLC in any state, work with your attorney etc. As with any third-party company offering you a service, please make sure to carefully vette their fees versus what you would pay to file the appropriate paperwork yourself directly with the state.

A. Human Resources is a critical administrative function for any small business owner especially if they have employees. Depending on your business structure and how large you anticipate it being you will want to determine quickly whether HR services are done in-house, whether you hire a consultant to set it up or if you want to outsource your HR to a third-party.

Please click here for eight common small business HR questions and answers. When first starting out, many small business entrepreneurs handle the HR themselves. However, as they expand and hire employees the HR issues become more complex with potential legal ramifications.

In fact, hiring employees requires a lot of attention to detail so it has been broken out (see below). Having an employee handbook, clear policies & procedures, clear understanding of local, state and federal laws and a properly instituted payroll management system in place before hiring the first employee can go a long way toward reducing staffing issues down the road.

I have a great idea or design for a business. Now what?

A. Absolutely. In order to protect your invention or work you need to go through a process. Depending on your business idea, service or product there are different types of protections for your intellectual property you can apply to receive.

Copyright

The U.S. Copyright Act, 17 U.S.C. §§ 101 - 810 , is Federal legislation enacted by Congress under its Constitutional grant of authority to protect the writings of authors. See U.S. Constitution, Article I, Section 8. Changing technology has led to an ever expanding understanding of the word "writings." The Copyright Act now reaches architectural design, software, the graphic arts, motion pictures, and sound recordings. See § 106. As of January 1, 1978, all works of authorship fixed in a tangible medium of expression and within the subject matter of copyright were deemed to fall within the exclusive jurisdiction of the Copyright Act regardless of whether the work was created before or after that date and whether published or unpublished. See § 301. See also preemption.

The owner of a copyright has the exclusive right to reproduce, distribute, perform, display, license, and to prepare derivative works based on the copyrighted work. See § 106. The exclusive rights of the copyright owner are subject to limitation by the doctrine of "fair use." See § 107. Fair use of a copyrighted work for purposes such as criticism, comment, news reporting, teaching, scholarship, or research is not copyright infringement. To determine whether or not a particular use qualifies as fair use, courts apply a multi-factor balancing test. See § 107.

Copyright protection subsists in original works of authorship fixed in any tangible medium of expression from which they can be perceived, reproduced, or otherwise communicated, either directly or with the aid of a machine or device. See § 102. Copyright protection does not extend to any idea, procedure, process, system, method of operation, concept, principle, or discovery. For example, if a book is written describing a new system of bookkeeping, copyright protection only extends to the author's description of the bookkeeping system; it does not protect the system itself. See Baker v. Selden, 101 U.S. 99 (1879).

According to the Copyright Act of 1976, registration of copyright is voluntary and may take place at any time during the term of protection. See § 408. Although registration of a work with the Copyright Office is not a precondition for protection, an action for copyright infringement may not be commenced until the copyright has been formally registered with the Copyright Office. See § 411.

Deposit of copies with the Copyright Office for use by the Library of Congress is a separate requirement from registration. Failure to comply with the deposit requirement within three months of publication of the protected work may result in a civil fine. See § 407. The Register of Copyrights may exempt certain categories of material from the deposit requirement.

In 1989 the U.S. joined the Berne Convention for the Protection of Literary and Artistic Works. In accordance with the requirements of the Berne Convention, notice is no longer a condition of protection for works published after March 1, 1989. This change to the notice requirement applies only prospectively to copies of works publicly distributed after March 1, 1989.

The Berne Convention also modified the rule making copyright registration a precondition to commencing a lawsuit for infringement. For works originating from a Berne Convention country, an infringement action may be initiated without registering the work with the U.S. Copyright Office. However, for works of U.S. origin, registration prior to filing suit is still required.

The federal agency charged with administering the act is the Copyright Office of the Library of Congress. See § 701 of the act. Its regulations are found in Parts 201 - 204 of title 37 of the Code of Federal Regulations.

For more information on copyrights please visit, Cornell University Law School website; the source for this material. For video presentations about copyrights you can visit Taking the Mystery Out of Copyright found through the Library of Congress.

Patents

A patent for an invention is the grant of a property right to the inventor, issued by the United States Patent and Trademark Office. Generally, the term of a new patent is 20 years from the date on which the application for the patent was filed in the United States or, in special cases, from the date an earlier related application was filed, subject to the payment of maintenance fees. U.S. patent grants are effective only within the United States, U.S. territories, and U.S. possessions. Under certain circumstances, patent term extensions or adjustments may be available.

The right conferred by the patent grant is, in the language of the statute and of the grant itself, “the right to exclude others from making, using, offering for sale, or selling” the invention in the United States or “importing” the invention into the United States. What is granted is not the right to make, use, offer for sale, sell or import, but the right to exclude others from making, using, offering for sale, selling or importing the invention. Once a patent is issued, the patentee must enforce the patent without aid of the USPTO.

There are three types of patents:

A) Utility patents may be granted to anyone who invents or discovers any new and useful process, machine, article of manufacture, or composition of matter, or any new and useful improvement thereof;

B) Design patents may be granted to anyone who invents a new, original, and ornamental design for an article of manufacture; and

C) Plant patents may be granted to anyone who invents or discovers and asexually reproduces any distinct and new variety of plant.

What Can Be Patented

The patent law specifies the general field of subject matter that can be patented and the conditions under which a patent may be obtained. In the language of the statute, any person who “invents or discovers any new and useful process, machine, manufacture, or composition of matter, or any new and useful improvement thereof, may obtain a patent,” subject to the conditions and requirements of the law. The word “process” is defined by law as a process, act, or method, and primarily includes industrial or technical processes. The term “machine” used in the statute needs no explanation. The term “manufacture” refers to articles that are made, and includes all manufactured articles. The term “composition of matter” relates to chemical compositions and may include mixtures of ingredients as well as new chemical compounds. These classes of subject matter taken together include practically everything that is made by man and the processes for making the products.

The Atomic Energy Act of 1954 excludes the patenting of inventions useful solely in the utilization of special nuclear material or atomic energy in an atomic weapon. See 42 U.S.C. 2181(a).

The patent law specifies that the subject matter must be “useful.” The term “useful” in this connection refers to the condition that the subject matter has a useful purpose and also includes operativeness, that is, a machine which will not operate to perform the intended purpose would not be called useful, and therefore would not be granted a patent. Interpretations of the statute by the courts have defined the limits of the field of subject matter that can be patented, thus it has been held that the laws of nature, physical phenomena, and abstract ideas are not patentable subject matter.

A patent cannot be obtained upon a mere idea or suggestion. The patent is granted upon the new machine, manufacture, etc., as has been said, and not upon the idea or suggestion of the new machine. A complete description of the actual machine or other subject matter for which a patent is sought is required.

For more information on patents and how to patent (or trademark) your invention/product please visit, The United States Patent and Trademark Office the source for this material.

Trademarks

A trademark is a word, name, symbol, or device that is used in trade with goods to indicate the source of the goods and to distinguish them from the goods of others. A servic emark is the same as a trademark except that it identifies and distinguishes the source of a service rather than a product. The terms “trademark” and “mark” are commonly used to refer to both trademarks and service marks.

Trademark rights may be used to prevent others from using a confusingly similar mark, but not to prevent others from making the same goods or from selling the same goods or services under a clearly different mark. Trademarks that are used in interstate or foreign commerce may be registered with the USPTO. The registration procedure for trademarks and general information concerning trademarks can be found in the separate book entitled “Basic Facts about Trademarks.”

A. For copyrighting your work visit, The U.S. Copyright Office or go through a private company such as Legal Zoom. It is vitally important if you are going to sell a product, design, artwork etc. you invented commercially to ensure it is copyrighted. Click here for fee schedule if applying through the U.S. Copyright office. Private copyright processors such as Legal Zoom will each have their own set of fees. Please make sure you are fully aware of the total fees to process your application.

To apply for a patent or trademark on your new invention please visit the United States Patent and Trademark Office. A list of fees to apply for a patent and/or trademark can be found at USTPO Fee Schedule.

Also, be cautious in utilizing third-party patent companies or individuals to assist you in applying for a patent. Make sure and research the company to ensure they are reputable.

Employees

Hiring Employees requires a lot of attention to detail to ensure you don't run afoul of local, state, federal or tribal law. Please refer the information below.

A. If you need or want employees there are a number of labor and employment laws and other criteria that may apply. Different subjects include:

Hiring your first employee

- Obtain an Employer Identification Number (EIN).

- Set up records for withholding taxes including Federal Income Tax Withholding, Federal Wage and Tax Statement and applicable state tax withholdings Oregon information found here.

- Employee Eligibility Verification. Visit the U.S. Immigration and Customs Enforcement agency's I-9 website for more information.

- Register with your state's new hire reporting program. For Oregon please visit herefor more information.

- Obtain worker's compensation insurance. For Oregon please visit here fore more information.

- Post required notices. Employers are required to display certain posters in the workplace that inform employees of their rights and employer responsibilities under labor laws. Visit the SBA Employment & Labor Law webpage for specific federal and state posters you'll need for your business.

- File your taxes. Generally, employers who pay wages subject to income tax withholding, Social Security and Medicare taxes must file IRS Form 941, Employer's Quarterly Federal Tax Return. For more information, visit IRS.gov. New and existing employers should consult the IRS Employer's Tax Guide to understand all their federal tax filing requirements.

- Get organized and keep yourself informed. Being a good employer doesn't stop with fulfilling your various tax and reporting obligations. Maintaining a healthy and fair workplace, providing benefits and keeping employees informed about your company's policies are key to your business' success. Here are some additional steps you should take after you've hired your first employee.

- Set up recordkeeping. In addition to requirements for keeping payroll records of your employees for tax purposes, certain federal employment laws also require you to keep records about your employees. The following sites provide more information about federal reporting requirements:

- Complying with standards for employee rights in regards to equal opportunity and fair labor standards is a requirement. Following statutes and regulations for minimum wage, overtime, and child labor will help you avoid error and a lawsuit. See the Department of Labor’s Employment Law Guide for up-to-date information on these statutes and regulations. Also, visit the Equal Employment Opportunity Commission and Fair Labor Standards Act.

A. Yes. Employee benefits play an important role in the lives of employees as well as their families. For that reason, the benefits you offer can be a deciding factor for a potential employee’s decision to work at your business.

There are two types of employee benefits must provide by law those the employer must provide by law and those the employer offers as an option to compensate employees. Examples of required benefits include social security and workers' compensation, while optional benefits include health care insurance coverage and retirement benefits. Both required and optional benefits have legal and tax implications for the employer.

This guide helps employers understand what they need to do to supply employee benefits required by law.

Social Security Taxes

Every employer must pay Social Security taxes at the same rate paid by their employees. The following sites from the Social Security Administration can help you comply:

- Information and Resources for Employers

- Social Security: Business Services Online

- Employer W-2 Filling Instructions and Information

- Instructions for Hiring Employees Not Covered by Social Security

- Guide to Oregon Business Taxes

Unemployment Insurance

Businesses with employees may be required to pay unemployment insurance taxes. If your business is required to pay these taxes, you must register with your state's workforce agency, which can be found on our State and Local Tax page. Oregon pages include:

Workers Compensation

Businesses with employees are required to carry Workers' Compensation Insurance coverage through a commercial carrier, on a self-insured basis, or through the state Workers' Compensation Insurance program. If you need or want employees there are a number of labor and employment laws and other criteria that may apply. Different subjects include:

Family and Medical Leave

The Family and Medical Leave Act (FMLA) entitles employees up to have 12 weeks of job-protected, unpaid leave during any 12-month period for any of the following reasons:

- Birth and care of the eligible employee's child, or placement for adoption or foster care of a child with the employee.

- Care of an immediate family member (spouse, child, parent) who has a serious health condition.

- Care of the employee's own serious health condition.

FMLA requires group health benefits to be maintained during the leave as if employees continued to work instead of taking leave. FMLA applies to private employers with 50 or more employees, and to all public employers. Visit the Department of Labor’s website for more information.

A. Yes. Independent contractors and employees are not the same, and it's important to understand the difference. Knowing this distinction will help you determine what your first hiring move will be and affect how you withhold a variety of taxes and avoid costly legal consequences. Please click here for more information. For Oregon please click here for more information .

A. While not required, pre-employment background checks can help employers make sure they are getting the best employees possible. However, there are a number of rules and regulations regarding pre-employment checks. Please visit the SBA Pre-Employment Background Checks page for more information.

A. The employee handbook is a vital communication tool between you and your employees. Please visit the SBA Employee Handbooks page for more information.

A. Creating an effective job description is an essential part of hiring and managing your employees. Job descriptions help employees understand their roles, chain of command and their job responsibilities.

Job Descriptions also:

- Help attract the right job candidates

- Describe the major areas of an employee's job or position

- Serve as a major basis for outlining performance expectations, job training, job evaluation and career advancement

- Provide a reference point for compensation decisions and unfair hiring practicies

For more information please visit the SBA Writing Effective Job Descriptions page.

Finances

First, the question you want to ask yourself is whether you want to be an expert in bookkeeping and/or accounting if those are not the focus of your business. If you are opening a clothing retail shop your focus, first and foremost should most often be on managing and leading that component. However, even should you choose to use a professional bookkeeper and/or accountant you must always be aware of your bottom line and ensure they are reporting the information to you accurately.

A. Top 10 "Do's" and "Do nots" of book keeping practices are:

Do's

- Even if you hire a professional to do your books, you should have a basic understanding of bookkeeping. If only to keep costs down you should know how to track your monthly income and expenses.

- Before you open the doors on your business, consult with an accountant that is familiar with your industry before you start.

- Determine what accounting software program works best for your business; there are many software program choices on the market.

- In the beginning, you may want to do your own weekly bookkeeping to help keep costs down and so you have an understanding of where your money is going.

- Depending on the type of business you own, determine whether you need to track inventory and implement internal controls to safeguard against potential loss of property.

- Take the time to reconcile your bank account on a monthly basis.

- Maintain a cash flow spreadsheet and update it at least weekly, using the bookkeeping software you’ve chosen.

- Outsource your payroll and payroll reporting to a payroll service provider; they have the skills to keep up with the myriad state and federal reporting that is inherent with payroll.

- Put together a financial statement (budget) at least once a month.

- Set up separate business bank accounts and keep your business records apart from your personal records.

Dont's

- Not “vet” the individual you may delegate check-signing authority to even if friend or family member.

- Never comingle personal and business assets – that includes cash.

- Use Money withheld for sales taxes, mortgage payments, sales taxes, etc. for other purposes.

- Hand off cash flow projections to someone else. You need to know the liquidity of your business.

- Be overly conservative in expense projections and conversely don’t be overly optimistic in your sales projections.

- Rely on a handshake or verbal agreement when it comes to making purchases for your business.

- Sit down and write checks for invoices without matching it to a purchase order.

- Wait until you’ve painted yourself into a financial corner before contacting a lawyer or accountant.

- Put off establishing a relationship with a banker until you need financing.

- Overlook seeking advice from your accountant and lawyer on important financial matters.Source

A. There are a number of different software packages you can utilize. It depends on a number of factors including what kind of business you have, whether you utilize Microsoft Windows, Apple OS X or a Linux OS platform. The most popular platform is the Microsoft Windows Platform for desktop accounting software. Another question is whether you want to utilize a cloud based accounting software program or a traditional desktop software program you can install on your computer. Some companies offer both options such as Intuit the makers of QuickBooks.

If you are interested in utilizing cloud based accounting software please note they have a number of advantages and disadvantages.

Cloud based accounting software advantages:

- You can access your data from anywhere at any time. The data is accessible via the internet so even if you are not at work or traveling you can access your data.

- You don't have to backup your data (though having a local computer backup copy of your data is a good idea) as the cloud based package has backups built in.

- You can upload data easily, including bank statements, to allow your bookkeeper and/or accountant to easily access your data more efficiently.

- You can have many users from different physical locations be able to access the same financial data simultaneously. No need to copy data to USB drive or try and email copies. This can greatly increase efficiency and let you make faster financial decisions.

- By not storing your data locally, you are better protected against disasters destroying your data such as natural disaster, viruses & hardware/software failures etc. You want to make sure you vet any cloud accounting company you choose to utilize to ensure they have adequate backup and security practices in place.

Cloud based accounting software disadvantages:

- Cloud based accounting apps require a good internet connection. No internet connection often means you can't access your data.

- The apps themselves are still immature compared to standard full desktop applications and as such don't have as many modules and/or reporting capabilities.

- They often have user and data limitations and are not always industry specific enough.

Please visit here for example cloud based accounting packages.

A. This is one area that many entrepreneurs are not sure about when starting a new business. There are a variety of factors to consider.

- What will be your total pre-operational expenses? For example, how much will you need to spend on equipment, inventory, licensing, supplies etc.?

- What are your expected monthly (and annual) operational expenses? This includes lease payments for location, business loan payments, utility bills, income taxes etc.?

- How much money do you need to generate monthly to pay for your personal expenses? In other words, how much profit does the business need to generate for you to pay your personal expenses? As a corollary question, how much cash savings do you have in-place that will not go into the business venture to ensure you will be able to pay your personal expenses? For example, let's assume your required personal income is $3,000 per month net to maintain your current lifestyle (and pay your bills). If you are not expecting to generate a profit for your business the first year (not have any salary for yourself) you will need to ensure you have a cash reserve of at least $18,000 to continue to pay your bills to live with the same lifestyle as before. One of the major issues with small business owners is overestimation of first and second year business revenue, underestimation of operational expenses and amount of capital (cash) reserves needed. This is why having a defined business plan and financial projections are so important when starting a small business. Not only are you able to narrow your focus but you are also able to identify if you will need to acquire additional outside funding to start your business so you don't have to close your business due to a lack of cash reserves.

Marketing

A. To run a succesful business, you need to learn about your customer, your competitors and your industry. Market research is the process of analyzing data to help you understand which products and services are in demand, and how to be competitive. Market research can also provide valuable insight to help you:

- Reduce business risks.

- Spot current and upcoming problems in your industry.

- Identify sales opportunities.

For more information and resources regarding marketing research and analysis you can visit the SBA

From Score.org 5 Marketing Must Haves for you to review.Download

A. Having a website allows you to reach a far broader market than you may otherwise be able to reach. While you may have a store location, by having a webiste; your company has a marketing presence 24 hours a day 365 days a year. Not just customers from your local geographic area may find your website but potential clients from all over the world. For those entrepreneurs who want to have a home business, having a website is a way to provide a "retail" storefront to your business without all the additional costs.

STBC offers a free online business directory listing to all CTSI enrolled tribal member business owners (from 1% to 100% ownership or if they are independent contractor). Please visit the Siletz Tribal Business Directory for more information.

Also, for more information on developing an online presence you can download the pdf below created by the SCORE organization and Go Daddy Online Webhosting and Domain Business.

Online InfoTechnical Questions

A. While you don't need a computer to run a business there are several advantages to having one. Having a computer allows a small businss owner to utilize productivity software such as Microsoft Office 365 Business and Adobe Content Creation Software. Accounting software (whether local or cloud based) allows the small business owner much more control over their business (see Finance section). Having a business email address and website are increasingly critical for a business to function under the current business climate.

If money is tight, there are also free alternatives to Microsoft Office that can open and save in the Microsoft Office formats to include Libre Office and Open Office.

When utilizing a computer for work purposes security becomes even more paramount. Things to do when utilizing a computer for work purposes:- Make sure you are using a fully patched Operating System that is still supported. For example, if you are still using Microsoft Windows XP or Windows 8 you are no longer protected from security holes and other risks as that operating system is no longer supported by Microsoft. You need to upgrade immediately to Windows 7, Windows 8.1 or Windows 10.

- Ensure all your software is up-to-date and patched. Many software applications have periodic security updates that you want to make sure you stay on top of to minimize your exposure. One example is java for your computer (needed by many programs and internet browsers and this website to function correctly). You want to ensure it is always up-to-date and remove all old versions. For Windows, you can click Free Java Download to get more information.

- Ensure you have an up-to-date antivirus package on your computer (Windows or OSx) that is run routinely.

- In Windows ensure you are not running your computer as an "Administrator" user. Always create a separate Standard User Account and only enter your Administrator password in when you are updating computer, installing software etc. By running as a standard user you decrease the ability for malicious software to install without your knowledge.

- In Windows, turn User Account Control (UAC) up to "Always Notify". While the popups that result may be annoying at first, you are able to review and approve everytime a program or setting requiring administrator access is activated. For most users UAC tends to occur a lot when computer is first being setup but after that it doesn't pop up nearly as often.

- For Windows PCs set the Data Execution Prevention (DEP) to "Turn on DEP for all programs and servcies except those I select". This helps increase security. Please Click Here for exact instructions. Should you notice a program not working correctly, you can try adding the program to the exception list.

A. This is critical! Always make sure you have up-to-date backups of your data both on-site and off-site. On-site data backups include utilizing a separate USB hard drive or Network Attached Storage (NAS) while off-site backups may include cloud based backup services such as Carboniteor Amazon Web Services.Think about what would happen if your personal computer or phone broke right now? Do you have backups of your critical financial information or your personal picture? The same holds true for business purposes. Always have an up-to-date backup!

Please note, for those utilizing or thinking about utilizing a RAID array; RAID is not a backup. RAID is utilized for redundancy; not backups!

A. More than 75% of data breaches target small and medium size businesses according to the Score Organization and Mcafee Internet Security" so it is important to ensure you are aware of cyber security if you have an online website and/or process payments online etc. For more information download and read the 10 Step Security Checklist below.

ChecklistHelpful Templates, Spreadsheets and Word Documents

You can visit www.bplan.com and/or www.score.org to get more Business Plan ideas and examples.

| Template Name | MS Excel/MS Word | |

|---|---|---|

| Sample Business Plan | Download | |

| Business Plan Template for Startup | Download | |

| Business Plan Template for Existing Business | Download | |

| 3 Years Of Income | Download | Download |

| 12 Month Cash Flow | Download | Download |

| Break Even Analysis | Download | Download |

Business Education/Resources

Our Native American Business and Entrepreneurial Network (ONABEN)

A nonprofit, public-benefit corporation created by Northwest Indian Tribes to increase the success of private businesses owned by Native Americans. ONABEN offers training and support focused on developing entrepreneurship in Indian communities. Programs are available to any Native American (regardless of tribal affiliation) and services are provided at local sites.

Oregon Coast Community College

For businesses in Lincoln County and for those considering starting or buying a new business, OCCC's Small Business Development Center (SBDC) can help. They offer free small business counseling to start-ups and established businesses, business development training, information and referral, and a Small Business Management program.

CTSI Education Funding

Siletz- Education Specialist

Alissa Lane 541-444-8373

Portland - Education Specialist

Katy Kaady 503-238-1512

Eugene - Education Specialist

Nick Viles 541-484-4234

Salem - Education Specialist

Sonya Moody-Jurado 503-390-9494

Oregon Cascade Council of Western Goverment (OCWCOG)

OCWCOG is a voluntary association of twenty cities, three counties, the Confederated Tribes of the Siletz Indians and a port district. Geographically, the OCWCOG spans a region from the crest of the Cascade Range to the Pacific Ocean and includes all of Linn, Benton and Lincoln counties.

OCWCOG helps communities collaborate to solve problems and connects member governments, businesses and individuals with a wide array of resources. By pooling resources through OCWCOG, services to the public can be provided more cost effectively and efficiently. OCWCOG also serves as a forum for cross-jurisdictional cooperation. Over the years, OCWCOG has assisted their members in a variety of areas.

Their business lending and economic development efforts aim to encourage new employment opportunities and promote a stable and diversified economy in the Southern Willamette Valley and Central Oregon Coast. They deliver professional commercial loan packaging, closing, servicing and collection services through various direct and indirect loan programs. They also provide administrative services, technical assistance and professional lending services through contractual relationships to local government and non-profit entities that offer economic development oriented commercial loans. The goal of their lending program is to foster economic development by providing access to capital for small business owners, for either start-up or expansion needs. This gives businesses the opportunity and capacity to play an important role in determining their futures. Ultimately it means the creation of more jobs in the communities they service. Please click the Business Referral Network PDF icon to get a list of key contacts in the Cascades West region of Benton, Lincoln and Linn Counties for common business development-reated queries.

Small Business Administration (SBA)

The U.S. Small Business Administration (SBA) was created in 1953 as an independent agency of the federal government to aid, counsel, assist and protect the interests of small business concerns, to preserve free competitive enterprise and to maintain and strengthen the overall economy of our nation. We recognize that small business is critical to our economic recovery and strength, to building America's future, and to helping the United States compete in today's global marketplace.

Although SBA has grown and evolved in the years since it was established in 1953, the bottom line mission remains the same. The SBA helps Americans start, build and grow businesses. Through an extensive network of field offices and partnerships with public and private organizations, SBA delivers its services to people throughout the United States, Puerto Rico, the U. S. Virgin Islands and Guam.

HUBZone Certification: The Historically Underutilized Business Zones (HUB-Zone) program was enacted into law as part of the Small Business Reauthorization Act of 1997. The program encourages economic development in historically underutilized zones through the establishment of preferences. The HUBZone program is in line with the efforts of both the Small Business Administration and United States Congress to promote economic development growth in distressed areas by providing access to more federal contracting opportunities. For more information please visit the link provided below.

Oregon Bizguide

For more information about starting a business in Oregon to include topics such as hiring employees, obtaining a Federal Tax ID Number, selecting a business structure, business name, tax Information and more the state of Oregon has a great online resource guide.

Business Oregon

Business Oregon is the state's economic development agency. Business Oregon works to create, retain, expand and attract businesses that provide sustainable, living-wage jobs for Oregonians through public-private partnerships, leveraged funding and support of economic opportunities for Oregon companies and entrepreneurs.

Oregon Native American Chamber (ONAC)

ONAC is dedicated to working with all members of the community to advance the educational and economic opportunities for Native Americans in Oregon and Southwest Washington.

Oregon Business SOS

The Oregon Small Business advocate is an independent voice for small business with the state government. Have trouble with a state agency? They can help you cut through the red tape and find a solution. Get information, get resources and get help at

Sample Business Books

Please see below for some business plan and small business startup resources. These are provided as examples only as there is a wide variety of books available. STBC does recommend all prospective business owners to review all the Business Planning and Business Education links here on the STBC website.

Debt to Income

Your debt to income ratio (DIR) is determined by your monthly income and your monthly expenses (bills). It helps to determine the capacity an applicant has to repay any borrowed funds. To calculate your DIR, first you total all your monthly expenses and divide that by your monthly income and multiply that figure by 100 to find your percentage of debt to income. You can calculate your DIR using the equation below:

Total of monthly expenses / monthly gross income x 100 = %

Example: you have $925.00 of monthly bills and your monthly income is $2,500.00

925.00/2,500.00 x 100 = 37%

Monthly Payment Calculator

Before applying for a loan whether through STRCP or another financial institution try our payment calculator to estimate your monthly payment: